Oh Kwasi, what did you do?

Show Me The Money

You are using an outdated browser. Please upgrade your browser to improve your experience and security.

A “mini-Budget” – a new one for me – was delivered last Friday and what followed was unbridled chaos (more on that in a moment), so much so that the nickname for the new Chancellor is KamiKwasi!

The Autumn Budget usually takes place around late October but due to the current cost of living crisis and looming recession, a mini-Budget was put in place to address this.

And then Kwarteng, seemingly fueled to address none of these things, must have decided that “why wait? Let’s get on with this recession” and announced tax cuts to favour the top 1% of taxpayers.

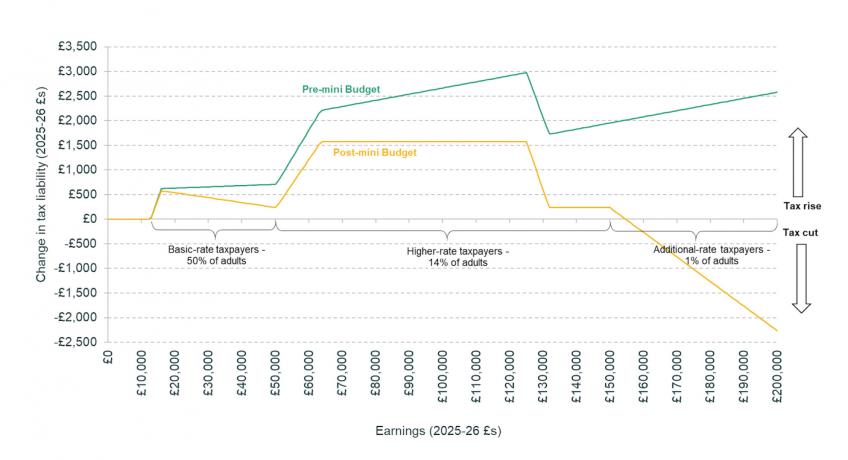

In short, those earning over £155k per year do well from this Budget, which represents 1% of UK taxpayers. And everyone else who earns below £155k, the 99%, well they don’t**.

** Despite cuts to the basic rate of income tax to 19% & reversal of the 1.25% Health & Social Levy from April 2023 and November 2022 respectively, inflation and the fiscal drag of not increasing the personal allowance and basic rate thresholds in line with inflation will cancel these out.

Nothing like reading the room at a time of national crisis but that’s what he did.

And then all hell broke loose, as he announced that in order to finance those massive tax cuts for those at the top of the pile, he’d be borrowing heavily.

And it hadn’t been costed by the OBR (Office for Budget Responsibility). A HUGE gamble, which the markets promptly decide they weren’t very impressed with. Who knew that fag packet, fingers in the air calculations coupled with hope don’t inspire confidence?

Cue a run on the £ not seen for several decades, skyrocketing interest rates on Government debt leading to the withdrawal of mortgage products in anticipation of rising interest rates (compounding the cost of living issues for anyone on a variable mortgage or soon to be variable mortgage) and the Bank of England launching a major intervention to prevent pension funds collapsing.

Even the IMF got in on the action and urged a rethink, whilst “closely monitoring” developments in the UK, as if the UK were an emerging economy.

So in the brief 10 minutes that he downed his Saki and nose-dived towards the aircraft carrier, these are our key points which have an impact on small & medium-sized businesses.

The top rate of tax (the additional rate) of 45% has been abolished from April 2023.

The threshold for where the top rate of tax kicked in was (and still is for 2022/23) £150k.

All very fortunate if you earn in excess of £150k, you might think.

However, it re-raises the tax planning opportunity from income distribution for all taxpayers, even those below the £150k level.

Yes, there needs to be commerciality in play here and no, your 18 year old full-time at University can’t get a £50k salary for 3 hours admin per term.

But there are options, both in limited company & sole trader business, to maximise your tax efficiency.

Remember, there is not just the basic rate, higher rate and additional rate in play here:

The plan was, from April 2023, that Corporation Tax rates would increase to 25% for limited companies with profits in excess of £250k, with a strange hybrid rate of 26.5% for profits between £50k and £250k.

In tandem with the proposed increase, there was an incentive to invest in new capital equipment by offering a 130% “super-deduction” before April 2023.

This gave you the same tax relief both pre and post-April 2023 and therefore encouraged you to invest early and not wait until the higher rate of Corporation Tax was in place.

This was simple maths, as 25% is roughly 130% of 19%. So on a £100k piece of capex, you’d get £24,700 of Corp Tax relief before April 2023 (£100k * 130% * 19%) compared to £25,000 (£100k * 100% * 25%) after April 2023.

So where are we going with this!? The super-deduction has been withdrawn from April 2023 but still applies until April 2023.

So on the same basis as above, the Corp Tax relief on capex pre-April 2023 will stay the same at £24,700 but post-April 2023, the same item will only attract Corp Tax relief of £19,000. A saving of £5,700 if it is purchased sooner rather than later.

If you’re planning any major capex purchases (remember, they have to be brand new and unused) in the next 12-18 months then it is well worth a call. Yes, there is the cashflow impact (or even borrowing cost) at an uncertain time but the tax-saving needs to be factored into the decision-making process.

There was not an abolishment of IR35 rules, as widely reported, but rather an abolition of “off-payroll working rules” from 6 April 2023.

This reverts the rules to the pre-2017 position, where workers providing their services via a limited company will once again be responsible for determining their own employment status and paying the correct amount of tax and NI, rather than the end user.

It will be important from April 2023, once again, for limited company directors to make sure they have correctly determined whether they are truly a subcontractor/supplier.

In all, not an official Budget, but certainly one of the biggest Budgets in a lifetime, with the biggest set of tax cuts in any Budget since 1972.

Only time will tell if the gamble will pay off or even if Kwarteng is still Chancellor by Christmas.

If you have any questions on the mini-Budget and how it may affect you and your business, please get in touch.

You can also find a useful mini-Budget factsheet here with all the main changes.