Spring Budget 2023

Show Me The Money

You are using an outdated browser. Please upgrade your browser to improve your experience and security.

Updated – please find our Spring Budget 2023 newsletter here.

It was an unusual Budget, largely devoid of any major tax changes since the tax plan had (in the main) been set in 2022’s Autumn Statement.

Despite pressure to do so, there was no backdown on the Corporation Tax rate increases or to the frozen personal allowances:

1. Corporation Tax – The Chancellor stood firm on the pressure to revisit the Corporation Tax rises which kick in from 1 April 2023. Until that date, all company profits are taxed at 19% but from 1 April, these change as follows:

2. Personal allowances – income tax and NIC thresholds are fixed until 2028 and we have talked previously about “fiscal drag” and the impact on personal taxes. In short, freezing the allowances for 8 years will bring in £30bn in extra tax and from this April brings £1.7m more people into tax and £1.2m more into higher rate tax.

The changes focus on a drive to bring more people into work (either returning to work or postponing retirement) and by bringing in investment in UK companies.

1. Pension changes

How much an individual can contribute to a pension is determined by two things; the available annual allowance and their level of earnings.

The maximum annual allowance has been increased from £40,000 to £60,000.

This is subject to tapering where the individual’s income exceeds two limits known as the Adjusted Income and Threshold Income:

The Adjusted Income was increased from £240,000 to £260,000, whilst the Threshold Income remains at £200,000.

For tapering to apply, both thresholds need to be breached, and where this happens, the £60,000 annual allowance is reduced by £1 for every £2 of Adjusted Income over £260,000 up to a maximum reduction of £50,000. Therefore, where the Adjusted Income is more than £360,000, the maximum annual allowance for the year is reduced to £10,000 (was previously £4,000).

The lifetime allowance limit has also been abolished (currently £1,073,000) however the maximum pension tax-free lump sum is frozen at 25% of the current lifetime allowance – this means that the maximum tax-free lump sum that could be taken from a pension is £268,250.

2. Capital expenditure for companies

With the end of the super-deduction period on 31st March 2023, there is a further attempt to incentivise business investment by introducing a “full expensing” allowance for the next three years.

Companies can write off unlimited expenditure on new capital items (cars and leased assets are excluded) and get tax relief at the rate they pay Corporation Tax.

This might seem very generous, but in practice will only benefit the largest 10% of companies. This is because an Annual Investment Allowance of £1m per year already exists for all businesses and 90% of businesses do not exceed the £1m spend per year of capital items.

3. Free Childcare

The Chancellor announced the increased availability of free childcare for all parents in an effort to increase the number of people in work.

This will be staged over the next 30 months:

Children will be eligible for 30 hours of care where:

Also be aware that the free hours of childcare are for 38 weeks of the year.

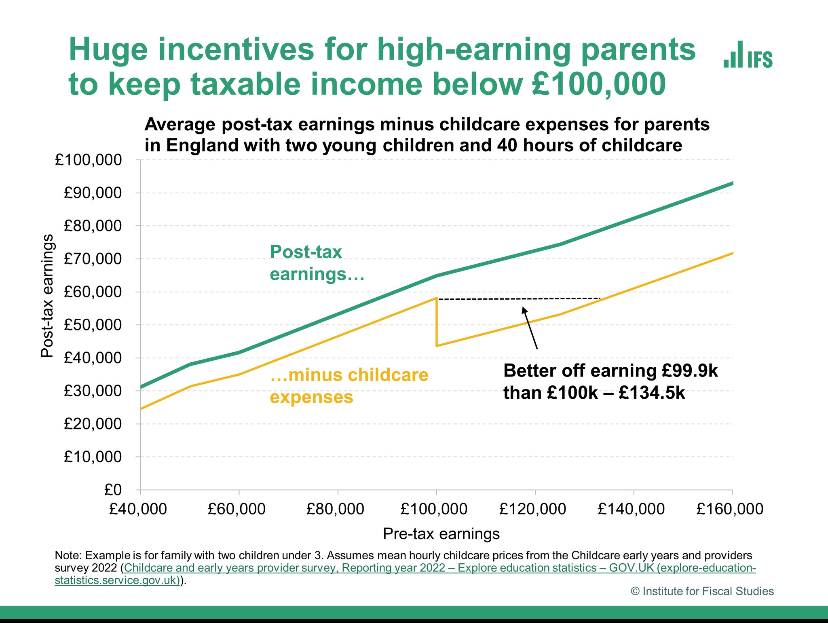

It is also worth noting a completely wild and insane tax situation that this childcare announcement has created.

If you take this example, of a parent with a 1 year old and a 2 year old, paying an hourly rate for 40 hours a week for childcare – they could see their disposable income fall by £14.5k if their pre-tax pay cross the £100k mark. A parent in this situation on £130k would be worse off than one earning £99.9k!

Now we don’t want to be too cynical but this seems a little less than encouraging!

We already have discussed the following tax events kicking in at the £100k mark and now there’s another disincentive to going over this level of earnings:

We’ve talked about tax planning opportunities to keep earnings under £100k (additional pension contributions, dividend timings and shareholdings etc.) and once again, this becomes an even more relevant conversation.

4. R&D

There has been a slight reversal of the reduced benefits to R&D due to come into effect from 1st April 2023.

Where a company has made a loss but made qualifying R&D expenditure, the 14.5% repayable tax credit has been reinstated (it was due to be reduced to 10%), but only where companies are “R&D intensive” – this means that 40% of expenditure is on qualifying R&D.

The reduction of the additional deduction for R&D expenditure (from 130% to 86%) will still go ahead.

We will be following up with a pdf Budget summary in the next few days.

If you have any questions on the 2023 Spring Budget, please get in touch.